The intensely competitive Chinese smartphone market witnessed a significant reshuffle in the first quarter of 2026, with domestic giant Huawei staging a remarkable comeback to claim the top position. This resurgence occurred amidst a slight contraction of the overall market, growing supply chain bottlenecks, and increasing cost pressures. The latest data, meticulously compiled and released by Omdia, paints a vivid picture of a market where local brand loyalty, strategic innovation, and premium segment appeal are dictating the leaderboard, starkly contrasting with the global landscape where Samsung recently dethroned Apple.

Global Shifts Versus Local Realities: A Tale of Two Markets

Just weeks prior, Omdia had published its global smartphone market report for the first quarter of 2026, revealing that South Korean behemoth Samsung had successfully reclaimed the global leadership from Apple, securing a robust 22% market share. This global victory for Samsung was widely reported and highlighted a strong start to the year for the company, pushing Apple into second place with a 20% share, followed by Xiaomi (11%) and OPPO (10%). However, the subsequent granular analysis of the Chinese market by Omdia unveiled a distinctly different narrative, underscoring the unique complexities and intense domestic competition that define the world’s largest smartphone arena.

The Chinese market, often seen as a bellwether for innovation and consumer trends, has consistently presented a formidable challenge for international brands, with local players often leveraging deep understanding of consumer preferences, aggressive marketing, and tailored product strategies. Samsung, despite its global dominance, has historically struggled to carve out a significant presence in mainland China, a trend that appears to persist into Q1 2026. Conversely, Apple, while relinquishing its global crown to Samsung, demonstrated surprising resilience and growth within China, while Chinese brands like Xiaomi faced significant headwinds.

Huawei’s Definitive Return to Leadership

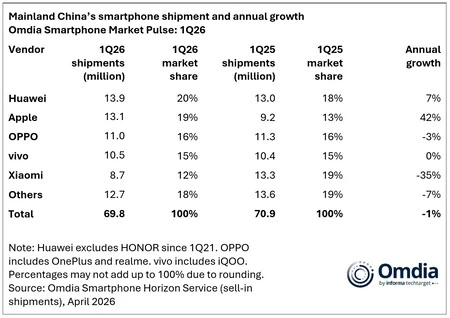

The most striking development from Omdia’s latest report is the emphatic return of Huawei to the top of the Chinese smartphone market. In Q1 2026, Huawei shipped an impressive 13.9 million units, securing a commanding 20% market share. This achievement marks a pivotal moment for the company, which has navigated years of unprecedented challenges stemming from stringent U.S. sanctions. These sanctions, imposed in 2019, severely restricted Huawei’s access to crucial American technology, including Google Mobile Services and advanced semiconductor chips, leading to a dramatic decline in its global and domestic smartphone shipments.

For years, Huawei, once a global leader, saw its market share dwindle as it grappled with supply chain disruptions and the inability to pre-install popular Android apps on its international models. However, the company doubled down on its domestic market, investing heavily in its proprietary HarmonyOS operating system and fostering a robust internal ecosystem. Furthermore, persistent efforts to overcome chip supply constraints, including leveraging domestic manufacturing capabilities and stockpiling components, appear to be yielding results. The re-emergence of its Kirin chipsets, even if in limited quantities, for certain premium models, has also resonated strongly with nationalistic consumer sentiment. Huawei’s strategic focus on premium flagships, coupled with its strong brand loyalty and extensive retail network within China, has been instrumental in its remarkable recovery, demonstrating the enduring strength of its brand among Chinese consumers. This resurgence not only solidifies Huawei’s position as a national champion but also intensifies competition across all segments of the Chinese smartphone market.

Apple’s Resilient Performance and Strategic Gains

In contrast to its global standing, Apple maintained a strong second position in the Chinese market during Q1 2026, shipping 13.1 million iPhones and capturing a 19% market share. While a slight dip from its peak performance in Q4 2025 – typically Apple’s strongest quarter due to new iPhone launches – the year-on-year growth figures are particularly noteworthy. Omdia’s data indicates that Apple managed to increase its market share in China by a remarkable 42% compared to the same period last year (Q1 2025).

This significant growth underscores the continued appeal of the iPhone brand and Apple’s premium strategy within China, even in the face of escalating domestic competition and a slowing economy. The launch of the iPhone 17 series in late 2025 likely provided a strong sales impetus that carried over into the first quarter of 2026. Apple’s robust ecosystem, perceived status symbol, and consistent user experience continue to attract a loyal customer base, particularly in higher-income urban areas. Despite geopolitical tensions and calls for greater support for domestic brands, Apple has effectively navigated the complex Chinese consumer landscape, maintaining its foothold and expanding its influence, often through strategic pricing adjustments, strong retail presence, and localized marketing efforts. Its ability to command premium pricing also positions it favorably against rising component costs.

Xiaomi’s Steep Decline: The Quarter’s Biggest Loser

While Huawei celebrated its return and Apple showcased its resilience, Xiaomi emerged as the quarter’s most significant underperformer in China. The company, which had been a dominant force in the Chinese market, slipped to fifth place, shipping only 8.7 million units and securing a mere 12% market share. This represents a drastic year-on-year decline of 35%. To put this into perspective, in Q1 2025, Xiaomi was the leading smartphone vendor in China, having shipped 13.3 million units and commanding a 19% market share.

This marks the fourth consecutive quarter of market share reduction for Xiaomi in its home country, signaling deep-seated challenges. Xiaomi’s traditional strength has been its value-for-money proposition, offering competitive hardware specifications at aggressive price points. However, this strategy appears to be facing increasing pressure. The resurgence of Huawei, with its strong domestic brand loyalty, and the consistent performance of other local players like OPPO and Vivo, have intensified competition in the mid-to-high range segments where Xiaomi has sought to expand. Furthermore, Apple’s continued success in the premium segment has limited Xiaomi’s upward mobility. The original article’s sub-note "Así es como gana dinero Xiaomi – te atraen y te atrapan" (This is how Xiaomi makes money – they attract and trap you) might hint at a strategy relying on ecosystem lock-in and ad-supported services, which could be less effective if the initial attraction of hardware sales falters in a crowded market. Xiaomi’s challenge moving forward will be to redefine its value proposition and differentiate itself amidst fierce domestic and international competition.

The Consistent Presence: OPPO and Vivo

Occupying the third and fourth positions respectively, OPPO and Vivo demonstrated steady performance in the Chinese market during Q1 2026. OPPO, which includes its sub-brands OnePlus and Realme, shipped 11 million smartphones, while Vivo followed closely with 10.5 million units. These companies have historically maintained strong distribution networks, particularly in lower-tier cities and rural areas, and have invested heavily in localized marketing and product development. Their diverse portfolios, catering to various price segments and consumer preferences, have allowed them to retain significant market shares. OPPO’s focus on camera technology and fast charging, and Vivo’s emphasis on design and audio quality, continue to resonate with specific consumer segments, ensuring their consistent presence in a highly dynamic market.

Underlying Market Dynamics and Economic Pressures

Beyond the individual company performances, Omdia’s report highlighted broader trends impacting the Chinese smartphone market. The overall market experienced a 1% year-on-year contraction, with total shipments reaching 69.8 million units in Q1 2026. This slight decline is attributed to several factors, chief among them the "aumento de los costes de los componentes, particularmente la memoria." The rising prices of key components have inevitably led manufacturers to increase the retail prices of their devices, a move that can dampen consumer demand, especially in an economy grappling with uncertainties.

The global semiconductor shortage, while easing in some areas, continues to impact specific component categories, driving up costs. The memory market, specifically, has seen volatility, directly affecting smartphone manufacturing expenses. This situation is further exacerbated by a cautious consumer spending environment in China, where economic growth has moderated, leading many consumers to extend their smartphone upgrade cycles. Instead of frequent upgrades, consumers are opting to use their devices for longer durations, waiting for more significant technological advancements or more favorable pricing. This confluence of rising production costs and tempered consumer demand creates a challenging environment for all smartphone manufacturers operating in China. The linked article in the original content, discussing China’s efforts to expand memory chip production, further underscores the strategic importance of this component and the broader implications of supply chain resilience for domestic manufacturers.

Implications for the Global Smartphone Landscape

The Q1 2026 results from China offer crucial insights into the evolving global smartphone landscape. Huawei’s comeback signifies the enduring power of domestic brands and the potential for companies to innovate and recover even under immense pressure. It also suggests that a dual-ecosystem approach (HarmonyOS vs. Android/iOS) could become a more prominent feature in certain markets.

Apple’s sustained growth in China reaffirms the strength of its premium brand positioning and its ability to weather market turbulence, setting a high bar for competitors aiming to penetrate the high-end segment. For Xiaomi, the steep decline in its home market poses a serious strategic challenge. While Xiaomi has aggressively expanded its global footprint, its struggles in China highlight the need for a robust and adaptable domestic strategy to fend off local rivals and maintain market leadership. The company will likely need to re-evaluate its product portfolio, pricing strategies, and brand perception in China to regain lost ground.

The broader market contraction and rising component costs indicate a maturation of the smartphone industry, where growth will likely be driven more by innovation, feature differentiation, and ecosystem integration rather than sheer volume. Manufacturers will need to balance cost efficiencies with consumer value, while navigating geopolitical complexities and a highly competitive environment. The Chinese market, with its unique blend of fierce domestic competition and strategic importance for global players, will continue to be a critical battleground shaping the future of the smartphone industry.